Layne is a Co-Host of the Calgary REI Hub Meetup, Real Estate Investor, and Mortgage Broker at Your Mortgage Team

Key Takeaways

- Saving a consistent amount monthly — even as little as $500 — and investing it over 30–40 years can produce life-changing wealth through compound growth.

- Lifestyle creep is one of the biggest silent threats to wealth-building. Split every raise: invest half, spend half guilt-free.

- Tracking your spending and net worth is the single most underrated financial habit — you can’t manage what you don’t measure.

- Trying to time the market is a trap. Waiting for the “perfect” deal or the “crash” costs you years of cash flow and equity growth.

- Rich and wealthy are not the same thing. Wealth is assets and cash flow — not how things look on the outside.

- House hacking is the most accessible entry point to your first investment property, requiring as little as 5% down.

- The BRRRR strategy — Buy, Renovate, Rent, Refinance, Repeat — lets you recycle capital and scale without needing a fresh down payment every time.

- Build a 3–6 month expense reserve per property. Vacancy, repairs, and rate changes are when, not if.

- Strong investors don’t just scale fast — they build portfolios that can survive the bad years.

Building a real estate portfolio doesn’t start with finding the right property. It starts with your relationship with money. Whether you’re trying to scrape together your first down payment or figure out how to grow from one rental to five, the habits and mindset you bring to your finances determine how far you go — and how fast.

At a recent Calgary REI Hub meetup, we broke down the money habits that make the biggest difference for new and experienced investors alike, along with the common mistakes we see over and over again, and a practical roadmap for going from your first property to a full portfolio.

Three Money Habits That Actually Work

1. Save Consistently — No Matter What

The single most powerful wealth-building move isn’t glamorous: save a percentage of your income every month and invest it. This idea has been around for a long time and has been implemented and taught by many.

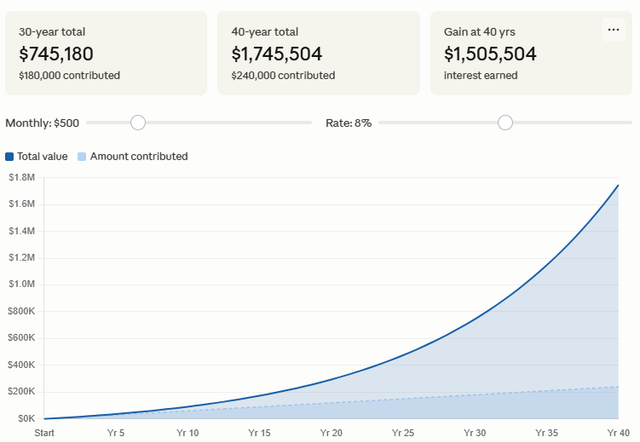

The math on this is hard to argue with. If you invest $500 a month at an 8% annual return:

- Over 30 years: approximately $745,000

- Over 40 years: approximately $1.5 million

And if you’re a real estate investor, $500 a month deployed into higher-return assets compounds even faster.

The challenge isn’t the math — it’s the habit. The key is to pay yourself first: automate your savings so the money moves before you ever see it in your account. If it’s already gone when you check your balance, you adjust your spending around it. If it’s sitting there, you spend it.

The point applies regardless of income. If you’re on a tight budget, start smaller — $50 a month, even $2 a day. The goal is to build the habit early, so that when income grows, the system is already in place.

2. Manage Lifestyle Creep — Don’t Let It Manage You

Lifestyle creep (also called lifestyle inflation) happens when spending rises automatically as income rises, leaving savings flat no matter how much more you make. We’ve seen clients go from earning $60,000 a year to $140,000 a year — and end up with the exact same amount of savings: zero.

The sneakiest form of lifestyle creep right now is food delivery apps. They’re frictionless. They’re always on your phone. And the cumulative cost is brutal. We’ve seen mortgage applications where people who aren’t earning a lot are spending 50% or more of their take-home income on delivery and eating out — without realizing it.

The solution isn’t to deprive yourself. It’s to be intentional. Here’s a simple approach:

- When you get a raise, take half of the increase and immediately route it to an investment or savings account before it hits your chequing.

- Let the other half genuinely improve your lifestyle — guilt-free. A vacation. Better food. Whatever matters to you.

- Since the investment is already handled, you never feel like you’re choosing between enjoying life and building wealth.

This also applies to big-ticket purchases. Vehicles are one of the most impactful financial decisions people make. If you lease a new car every three years versus buying a three-year-old vehicle and driving it for three or more years, the difference in net worth over a career can be significant — one study puts it at retiring up to 12 years earlier for the used-car buyer.

That said, if you love cars and they’re a genuine priority for you, there’s a smart way to handle it: use investment returns to fund lifestyle upgrades. Find a property, add value to it, and let the cash flow cover what you want. That way you’re building net worth and enjoying the reward at the same time.

3. Track Your Spending — And Your Net Worth

This one’s uncomfortable for a lot of people. But it’s the most clarifying thing you can do.

When you don’t track, you have no idea where your money is actually going. We’ve seen people genuinely shocked to discover how much they’re spending on things they don’t even think about — takeout lunches, subscriptions, delivery apps. One case involved spending 55% of take-home income on food delivery alone. As soon as it was tracked and made visible, it changed immediately.

The same principle applies to your net worth. A lot of people avoid tracking it because they’re worried about what they’ll see. But what we find is the opposite — tracking creates momentum. Watching a negative number get less negative, then cross into positive territory, becomes motivating in a way that abstract goals can’t match.

For investors, net worth tracking is especially valuable. It’s easy to feel like nothing is changing when you’re managing tenants and dealing with weekend renovations. But when you actually sit down and calculate that three mortgages are being paid down at, say, $1,200 each per month — that’s $3,600 a month, $43,000+ a year in equity building — even before appreciation. Tracking makes that visible.

Tools are simple. A spreadsheet works fine. Pull your bank and credit card statements and work backwards for the last few months. You’ll find out quickly where the leaks are.

Common Money Mistakes to Avoid

1. Trying to Time the Market

This is one of the most common reasons people never actually buy their first property. The logic sounds reasonable: wait for prices to drop, then buy low. In practice, it rarely works out that way.

While you’re waiting for the crash, properties that were bought are generating cash flow and building equity. And if you’re speculating on prices going up, you’re exposed to the same risk as pre-construction condo buyers in places like Toronto, where many investors are currently underwater because they bought on the assumption prices would keep rising.

We’ve also seen people spend five years searching for the “perfect deal” — and miss out on what would have been solid, profitable investments. A decent deal five years ago and the equity that comes with it beats the perfect deal you’re still looking for today.

The same caution applies to get-rich-quick schemes. If it looks too good to be true, it almost always is.

2. Confusing Looking Rich With Being Wealthy

Rich and wealthy are not the same thing, and the difference matters enormously as an investor.

Someone who looks rich — fancy car, nice clothes, regular vacations — may have a high income and zero assets. Someone who is wealthy may not look flashy at all, but they have cash-flowing investments, assets that appreciate, and the option to stop working if they choose.

We see this regularly when people come in to finance an investment property. They appear to have money. Then we look at the numbers and they’re spending everything they earn. No room to qualify.

3. Ignoring the Difference Between Good Debt and Bad Debt

Debt itself isn’t the enemy — bad debt is. Car loans for depreciating vehicles, credit card balances used for lifestyle spending, lines of credit funding consumption: these cost you money and build nothing.

Good debt — specifically, leveraged mortgages on income-producing properties — is a tool. It lets you control more assets than you could own outright, and someone else (your tenants) helps pay it down over time. The key is keeping leverage at a level that doesn’t expose you to forced selling if things get difficult.

4. Underestimating the Time Value of Money

Every dollar you spend today is a dollar that can’t compound. That’s not a reason to never spend money — it’s a reason to be deliberate about it.

The numbers are stark. Starting to invest $500 a month at age 25 rather than age 35 can result in roughly $1 million more by age 65, illustrating the powerful impact of time and compound growth. That’s the power of compounding, and why Warren Buffett’s track record is as much a function of how long he’s been investing as how well.

How to Get Into Your First Investment Property

Once the habits are in place and savings are building, the next question is how to get into the market, especially if you’re cash-tight or have qualifying challenges.

1. House Hacking

The most accessible entry point for most people is house hacking. The idea is simple: purchase a property as a principal residence (which lets you put as little as 5% down), move into part of it, and rent out the rest to offset your living costs.

This gets you into the market sooner, starts building equity, and often significantly reduces what you’re paying to live somewhere. The longer runway you have as an investor, the better the long-term outcome.

2. Partnering Up

If qualifying is the barrier, partnering with someone — a family member, a co-signer, or someone from an investor network — can bridge the gap. Getting into a property earlier almost always beats waiting to do it alone.

3. Creative Financing

When traditional financing isn’t an option, there are alternatives worth exploring: agreement for sale, vendor take back (VTB) mortgages, and other structures that allow you to acquire a property without a conventional mortgage.

For a detailed breakdown of how these structures work, check out our meetup session with real estate lawyer Scott Bollinger on our YouTube channel.

Getting into your first investment property can be as simple as having a conversation with us. Book a consultation today!

Scaling Your Portfolio: Forcing Appreciation

Once you own a property, natural appreciation happens over time — but waiting for it is slow. To scale a portfolio faster, you need to force appreciation through strategic action.

Value-Add Improvements That Actually Work

Not all renovations are equal. The goal is to increase rental income or property value — not just make something look nicer. High-impact moves include:

- Adding a legal basement suite to a property with an unfinished basement

- Adding a garage or garage suite where the lot allows

- Strategic renovations that lift rents to current market rates

- Room rentals (if that structure works for your situation)

One common mistake newer investors make: buying the cheapest materials. The doorknob that starts sticking in three years, the laminate flooring that needs replacing in five — these false economies cost more in the long run. Spending a bit more upfront on quality materials reduces maintenance costs and keeps properties competitive.

Another overlooked move when buying a tenant-occupied property: if previous rents are below market, work toward getting them to current rates. That rent gap is often where a significant chunk of a deal’s potential is sitting.

The BRRRR Strategy

For investors looking to recycle capital and grow without needing a fresh down payment every time, the BRRRR strategy is worth understanding.

Here’s how the cycle works:

- Buy a property that’s undervalued or has clear room for improvement.

- Renovate strategically — add a suite, improve finishes, raise the property’s income potential.

- Rent the property at top market rents.

- Refinance with a lender at up to 80% loan-to-value. The lender now values the property based on the improved income and condition.

- Repeat — use the equity you’ve pulled out to go buy the next property.

A realistic note for Calgary: a perfect BRRRR — where you recover 100% of your invested capital — is difficult to pull off here. You’re unlikely to get all your money back out. But you can typically access a meaningful chunk of it, enough to accelerate your next acquisition without starting from zero.

In Calgary, BRRRR tends to work best in older, established communities on larger lots — places like Fairview, Acadia, Bowness, Huntington, and Beddington. Newer suburban developments outside the ring road generally don’t have the same value-add potential. Bungalows and bi-levels tend to be the best candidates for this strategy.

Weathering the Storms: Building a Resilient Portfolio

Calgary’s real estate market is cyclical. It’s tied to oil and gas prices, employment trends, and broader economic conditions. Building a portfolio that only works in good times is not really building a portfolio — it’s speculating.

Keep a Reserve

Set aside 3–6 months of expenses per property and keep it separate. This covers:

- Vacancy: Vacancy rates in Calgary have been rising, particularly in the suburbs for detached properties and basement suites, and even higher for condos in the downtown core.

- Unexpected repairs: Roofs fail. Furnaces die — and somehow, always on a long weekend or a holiday. A $6,000 furnace replacement on Christmas Eve is a real scenario, not a hypothetical.

- Interest rate changes: Rates have moved significantly in both directions in recent years. Your portfolio needs to work across a range of rate environments.

Stress Test Your Numbers

Before any acquisition, run a worst-case scenario: What if rents drop 15%? What if prices drop 10%? What if the property sits vacant for two months? If the answer to “can I survive this?” is no, you need a plan before you buy — not after.

Right now, rents are softening across Calgary — in some areas more than others. Factor that into your projections. Conservative underwriting today means you’re not forced to sell under pressure later.

The investors who come out ahead through market cycles aren’t necessarily the ones who bought the most properties. They’re the ones whose portfolios held together when things got hard.

Conclusion

Building a real estate portfolio in Calgary isn’t complicated. But it does require honesty, consistency, and the willingness to start before everything feels perfect.

The investors who get there aren’t the ones who found a secret strategy. They’re the ones who automated their savings before lifestyle caught up, tracked their numbers when it was uncomfortable, and bought a decent deal instead of waiting forever for a perfect one. They built reserves before they needed them. They stress-tested their portfolio before the market did it for them.

The path is the same whether you’re trying to scrape together your first down payment or figuring out how to scale from two properties to five. Get your money habits sorted. Get into the market. Add value where you can. Build a portfolio that survives the hard years, not just the good ones.

You don’t need to do this alone either. The REI Hub exists because real estate investing is a team sport. The right mortgage broker, the right legal advice, the right investor community around you can cut years off your learning curve and thousands of dollars off your mistakes.

If you’re ready to take the next step, whether that’s your first property or your next one, book a consultation with our team. We’ll look at your numbers, talk through your options, and help you figure out where to move from here.